The US Debt and Deficit

Remember the shocking news that the US deficit was scheduled in 2020 to hit $1 trillion?

It was an unbelievable number and certainly alarming to those that believe less debt is better than more debt. With the virus crisis and miscellaneous stimulus packages now in place (and more to come), the new deficit totals this year will be staggering.

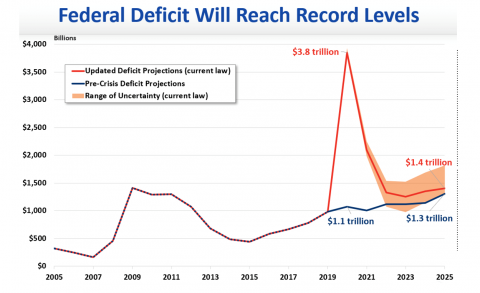

The deficit this year will likely be somewhere in the neighborhood of $3 to $4 trillion. As you can see from the chart below, this is a significant increase that will be added to the overall debt of the United States.

http://www.crfb.org/blogs/new-projections-debt-will-exceed-size-economy-year

US Currency is Still Strong

The good news for the United States is that our currency is currently trusted. The printing of money still does not have an immediate impact on the US dollar as it is the respected currency in the world. But it is fair to wonder how long this can continue if debt levels continue at a high level.

Still, while the US may have huge debt loads, many other countries around the world are struggling with the same problem. It’s not just the United States. On a relative basis, we are looking fairly solvent.

No Appealing Alternative

It would be easy to say that eliminating debt and just letting the economy float along with a laissez-faire perspective would be an appropriate free-market strategy. But one must understand very clearly what this type of path entails. If one was not to insert stimulus packages from the Federal Reserve and the US government, we would actually see an economic downturn that none of us have ever experienced. The economy would grind to a halt and the damage would be severe.

For that reason, most economists believe the US debt levels taken on during this viral crisis are a reasonable action to soften the blow from our shelter in place existence. You will note from the chart that it is expected that annual deficit levels will return post 2020 to more normalized levels (if you consider $1.3 trillion deficits normalized).

On an overall basis, the United States is adding $3 trillion onto the already existing $21 trillion deficit. The percentage increase is about 15% which doesn't quite sound so bad when one looks at it from that perspective. There's not much that can be done about deficits right now. There is an appetite to avoid financial collapse and so this year deficits will be unprecedented.

Debt Consequences

There will be consequences related to high US debt levels. We can expect slower GDP growth, impacted standard of living, and less governmental financial flexibility as the government continues to pay huge annual interest costs. Those costs right now, since interest rates are so low, are manageable. They become more problematic if interest rates rise.

I do not believe that high debt levels will lead to a one-time economic collapse. Instead, I believe GDP growth will grow less than it could have because of high deficits on an annual basis. This incremental growth headwind won't feel so disturbing as just a bit of it happens on an annual basis. But add it all up over a ten-year period and you will see that the result is a significant 10-year economic headwind. We are investing based on this perspective.

Portfolio Strategy

I believe it is important to look down the road to see what portfolio strategy consequences might look like because of actions taken today. Our DWM Research team is hard at work every day analyzing and assessing the impact of current headlines.

DWM portfolio strategies assume high future debt levels in the United States. The assets we invest in are on the assumption that the US economy will grow but at a slower rate because of debt. Equity and fixed income investments reflect our viewpoints that industries that have tailwinds, as well as companies that have strong balance sheets, will likely do well. Dividends will matter.

We will get through this. The United States will come out of this downturn because fundamentally the US economy is still sound despite this horrible pandemic. When we get a treatment and a vaccine, you'll see an economic recovery; its coming. The bumps might be tough this year, but recovery will come.

The opinions expressed herein are provided for informational purposes only and are not intended as investment advice. All investments involve risk, including loss of principal invested. Past performance does not guarantee future performance. Individual client accounts may vary. Although the information provided to you on this site is obtained or compiled from sources we believe to be reliable, Destination Wealth Management cannot and does not guarantee the accuracy, validity, timeliness or completeness of any information or data made available to you for any particular purpose. Any links to other websites are used at your own risk.