U.S. Deficit

You may be aware that the US deficit is large and growing larger by the day. While we do not expect this to crash the economy near term, it certainly is an economic headwind for economic growth. An article published in July 2020 by the Brookings Institute outlined some issues related to the federal deficit. See a few excerpts below:

***

Begin quote

How worried should you be about the federal deficit and debt?

By David Wessel

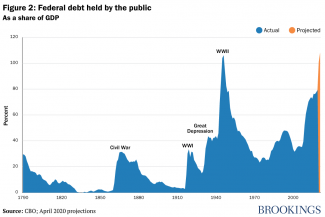

Even before the pandemic, the federal deficit was large by historical standards and projected to rise. The sharp recession and the spending increases that Congress and the president approved in response has made the deficit even bigger. Big deficits mean a growing federal debt—the total the government owes—already at its highest point since World War II. Extraordinarily low interest rates allow the U.S. to shoulder a heavier debt burden, but the debt is on an unsustainable course and its size may limit the government’s ability or willingness to continue to fight the economic ill effects of the pandemic or future economic downturns.

- At 17.9% of GDP in Fiscal Year 2020, the federal deficit is almost twice as large than at the worst of the Great Recession in 2009.

- The federal debt, measured against the size of the economy, is larger than at any time since the end of World War II and is rising.

- The U.S. government spends as much on interest as the combined budgets of Commerce, Education, Energy, DHS, HUD, Interior, Justice & State.

What is the budget deficit?

The deficit is the difference between the flow of government spending and the flow of government revenues, mainly taxes. For fiscal year 2019, which ended September 30, 2019, total revenues were $3.5 trillion (up 4% from the previous year) and total spending was $4.4 trillion (up 8% from the previous year). The resulting deficit was $984 billion (4.6% of gross domestic product) compared to $779 billion (3.8% of GDP) in the previous year.

When the coronavirus pandemic hit in early 2020 and the government ordered a lockdown of much of the economy, Congress responded with substantial spending to ease the pain. The combination of the deep recession (which automatically leads to less tax revenue and more spending on programs like Medicaid and food stamps) and the spending Congress appropriated in response to the pandemic increased the deficit significantly. The Congressional Budget Office projected in April 2020 that the deficit for Fiscal Year 2020 will be at least $3.7 trillion, or 17.9% of projected GDP, and it could be even larger if Congress approves more spending increases or tax cuts in light of the pandemic.

Is that considered a large deficit?

Yes. By any measure, the projected 2020 deficit is very large. Deficits over the last 50 years have averaged just 3% of GDP. Even during the Great Recession, the largest deficit recorded (in Fiscal Year 2009) was just 9.8% of GDP. Even though the economy was reasonably strong before the pandemic hit, the deficit was already elevated by historical standards, largely because of the big 2017 tax cut. The COVID-19 recession and the congressional response to it have caused it to balloon.

Measured against the size of the economy, the debt was around 35% of GDP before the Great Recession of 2007–09 and had risen to nearly 80% of GDP right before the pandemic. It’s headed to around 100% of GDP by the end of Fiscal Year 2020 on September 30, and—barring a major change in tax or spending policy—it will keep rising after that to levels never before seen in U.S. history. (The record was set during World War II in 1946, at 106.1% of GDP.)

End quote

***

Source:

https://www.brookings.edu/policy2020/votervital/how-worried-should-you-be-about-the-federal-deficit-and-debt/

I was asked today if I thought the US deficit would crash the US economy in one cataclysmic moment. My answer was that I do not expect a one-time moment where suddenly everything crashes because of high debt levels. What I do expect is substandard growth on the long term because of high debt servicing expenses that must be paid for by the federal government. Higher debt payments mean lower government investment in the economy to stimulate economic growth.

We are investing based on the assumption that growth will be substandard for the next 5 to 10 years for a variety of reasons including high deficits and demographic changes. We've adjusted our portfolio strategy perspective consciously as we simply do not believe that the deficit will be attacked in any meaningful way in the near future.

The opinions expressed herein are provided for informational purposes only and are not intended as investment advice. All investments involve risk, including loss of principal invested. Past performance does not guarantee future performance. Individual client accounts may vary. Although the information provided to you on this site is obtained or compiled from sources we believe to be reliable, Destination Wealth Management cannot and does not guarantee the accuracy, validity, timeliness or completeness of any information or data made available to you for any particular purpose. Any links to other websites are used at your own risk.