U.S. Dollar Q&A

I'm sure you have noticed the increasing number of headlines concerned about the strength of the U.S. dollar. This is understandable given the tremendous level of debt that the U.S. government incurs each year.

It's right to wonder if that means doom for the U.S. dollar. I don't think so. See a couple questions I was asked recently. Hopefully, this sheds a bit of light on our perspective.

- Should investors be concerned about protecting their portfolios from a potential major devaluation of the U.S. dollar?

I think devaluation is certainly a concern because of the skyrocketing debts. Essentially the United States is skating by at this point because credit ratings are still high, and the U.S. treasury is still considered the safest investment in the world. When the market panics people buy U.S. treasuries.

The real question is what this will look like down the road. I think that there is a risk of the dollar being negatively impacted if debt continues to spiral out of control. While I think this is a legitimate concern, I think it's a concern that will really play out more along the 10-to-15-year timeline. So, in essence is our children's problem in some ways which is horrible to say.

In the meantime, I expect the U.S. dollar to still be the world currency.

- How significant is the rise of the Chinese yuan as a global trade currency, especially as more countries like Brazil, Russia and India begin accepting it in transactions?

I do not believe the Chinese yuan anytime soon will be a currency reserve. While I realize BRIC (Brazil, Russia, India, China) countries have been trying to somehow band together, we believe them to be disastrous economies. I also think that there would be considerable resistance about replacing the U.S. currency with the Chinese currency from a geopolitical basis. Remember, China's shadow banking system has had massive declines in real estate values impacting these off the balance sheet loans. So, in other words, the strength of Chinese economy in my view is an illusion that has a transition to more of a consumption economy.

- How does the U.S.'s reliance on foreign financing of its debt compare to countries like Japan, which largely finance their debt domestically?

See above. I don't expect the U.S. not to be the reserve currency and I think we are much different then Japan. Japan has several things going against it, including demographics and a failure to address real estate concerns and bank debt. They didn't have a financial crisis like we did. They massaged their financial crisis over a 25-year period and that's why the economy has suffered so much.

- Could the unpredictability of U.S. international policies such as tariffs and changes in global program funding pose a long-term risk to the dollar’s strength?

Especially nowadays, this is a concern. But I believe the dust will settle on trade policy and when it does a new normal will settle in. I don't think it will negatively affect the dollar. It will likely negatively affect inflation and perhaps economic growth, but in terms of currency strength, I don't think it will have a lasting impact.

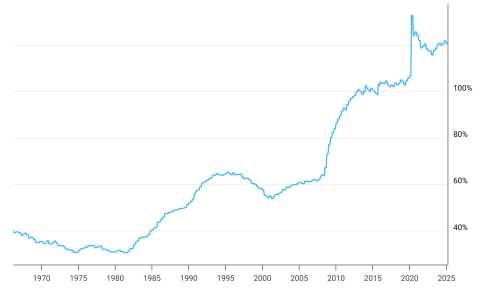

- What are the implications of the U.S.’s rapidly growing national debt, especially when compared to debt levels in other major economies?

It's a new debt economy perspective that most countries are adopting. But I do find it concerning as referenced in my point above. The U.S. federal debt now exceeds 120–125% of GDP, one of the highest levels in modern history.

Source: https://www.macrotrends.net/1381/debt-to-gdp-ratio-historical-chart

Although our investments are diversified and large cap U.S. companies are mostly international, it is not clear to me how those factors are a defense against devaluation.

Something that often is not talked about is a secret positive of the dollar becoming weaker. Multinational companies based in the U.S. send out products and they are purchased in foreign economies. That money eventually is repatriated back into U.S. dollars. In other words, companies that are diversified, international companies will benefit from a weak dollar because it will help earnings. It's one of the reasons that we do invest in global assets, because we do believe that international markets will give us a tailwind regarding the earnings of companies we hold in your portfolio. To give you an idea of the equities in your portfolio, over 50% of the revenue comes from international sales. This is a multinational tailwind that will benefit the earnings of those companies. Better earnings mean better asset prices going forward.